I haven’t read the pleadings, but it sounds like the lack of standing could easily doom this case. That said, this case arises out of the universities’ lack of transparency regarding how financial aid is awarded. From Ms. Donahue’s 2008 statement, there certainly is the appearance that the schools are working against the interests of students. We don’t know what we don’t know. It would be nice to know.

1 Like

If the 1991 consent decree is any precedent, you can be sure there will be an unintended consequence of some sort, similar to FA applicants no longer being able to apply ED anywhere with any degree of certainty that their awards would be “the best deal” compared to their RD choices. This was not a huge concern before the decree; now, it is.

The above is a column from the NY Times on this lawsuit. Apparently the section 568 is valid through September 30, and would need another extension to remain valid. So even if this lawsuit doesn’t become a big class action lawsuit, it may do enough damage to get the exemption removed.

1 Like

Unfortunately, this article is behind a paywall.

Anyone willing to summarize the article ?

See if this link works for you.

3 Likes

I read it. It’s just what people have said already, a heads-up that the sec.568 extension will probably not be renewed. The reason given is mostly backlash against wealthy elite institutions in general. Let’s face it, there is no natural constituency for the Ivy League nor any other form of aristocracy in this country.

1 Like

Thank you, but the paywall still appears.

I would pay, but I have difficulty keeping track of all of my passwords as it is.

On second thought, the NYT & Wash Post & Wall Street Journal & several other newspapers (Pittsburgh & Los Angeles) are worth it.

Thank you again.

There’s a share/gift this article option and I wondered if it might work.

1 Like

I wouldn’t be sad if the schools had to set their own tuition and FA formulas. I don’t really feel bad for a kid who has to go to Dartmouth because Harvard didn’t give them the same aid, or if a student has to pick between Princeton and Vandy because one costs less. Montana doesn’t meet with NM to set tuition rates and FA formulas, so why should the elite colleges get to do that? If Harvard thinks its education is worth $150k, they should charge that even if Yale is only charging $80k.

3 Likes

Update on this lawsuit…DOJ files brief (but did not join case) basically supporting plaintiffs.

The colleges accused of violating antitrust law defend their action by citing the “568 Exemption” for colleges that admit all their students in a need-blind way. But the Justice Department says that “an agreement between schools that admit all students on a need-blind basis and schools that do not is beyond the scope of the 568 Exemption. Thus, to the extent that at least some of the defendants do not admit all students on a need-blind basis, the 568 Exemption would not apply here.”

1 Like

I have not read all of the posts in this conversation, but I remember the news story when it first came out earlier this year. I think that I get the gist of the plaintiff’s complaint, but the part that puzzled me at the time is why the colleges on the list offer such different aid packages if they are colluding on FA.

When my daughter was crafting her application list last fall, we ran the net price calculator at 25+ different colleges including seven from the lawsuit’s list. The results varied pretty wildly for expected family contribution. In general, from her first pass list of reaches, targets and likely colleges, NPCs ranged from 4K-20K. However, focusing on the seven schools that she was considering from the sixteen on the lawsuit list, the NPC ranged from an EFC of 4500-12500.

By the way, while the schools from the lawsuit were at the lower end of the original 25ish, all but one estimated prices that were higher than the small liberal arts colleges that she was originally considering (Grinnell, Colby, Bowdoin, Williams, Haverford, Amherst, Trinity in CT…). Incidentally, there was also a wild variation between what was listed as parent contribution vs. student contribution, but I considered that issue less important than the total family contribution. The majority of the schools (including the one that gave us the 12500 estimate) did not have loans as part of their packages, but she/I would have had to borrow to make several of the packages work.

Why such variation from the lawsuit colleges when they collude on the formula itself? Note, I am not doubting that they coordinate since the colleges admit that upfront. I am just confused at why the numbers are so radically different. I know the NPC is a somewhat blunt instrument, but I would have thought that given the collusion and the bluntness of the instrument, those estimates from lawsuit schools would have been clustered closer together even if the actual packages offered in April were further apart.

I can’t do a post admission comparison since she only ended up applying to one school from the lawsuit list. The final aid package was pretty close to what had been estimated but so were the packages from the schools not on the lawsuit list.

3 Likes

Even though these schools all belong to Group 568, that doesn’t mean their FA formulas are the same. For example, some of these schools include home equity in their calculation (so a %age gets included in the family contribution), while others don’t. I am sure others who have worked in FA can cite more examples.

I am far from an expert in this case, but all along I thought the schools may not have much of a case, as many of the named schools are need aware for international students. Other students for whom they may know their level of need during admissions include athletic recruits, development admits, and QB and Posse applicants. And that doesn’t include how they use CollegeBoard’s Enviromental Context Dashboard and/or other factors as proxies for gauging income/asset levels. Need blind doesn’t seem an accurate descriptor anymore.

If multiple colleges have similar net prices, how much of the net price is allocated to student contribution can matter in some ways:

- A higher student contribution may include more work-study eligibility, meaning a preference for some on-campus jobs that has a larger effect.

- Many colleges allow outside scholarships to reduce student contribution before reducing their own grants. If such a college lists a higher student contribution, that can allow for a larger amount of outside scholarships to reduce the total net price.

1 Like

Good point. You are totally right. I had forgotten about the above considerations. To be honest, they didn’t play an issue in deciding where to apply because we weren’t thinking that granularly. However, #2 weighed on our minds in deciding where to commit. It made more sense to choose the school that had a relatively higher student contribution and a lower parent contribution becuase of the way schools handle outside scholarships --they wouldn’t (couldn’t by law?) reduce my parent contribution, but they could reduce expected work study, summer work and student loans. It wasn’t the only deciding factor, but we definitely thought about it since by the time she was getting ready to commit, she already knew about her outside scholarships.

1 Like

DOJ is saying that they support the theory of the case. They’re not saying the plaintiffs have proven their case. Given the complexity of the argument, a dismissal would have been highly unlikely at this juncture.

One thing that has affected what college costs is the changes to the EFC formula over time. There’s a bit of chicken and egg to explain if the schools’ higher cost was pushing the formula or the formula’s extra money was fueling the price jumps, but the formula has been taking more from families for years.

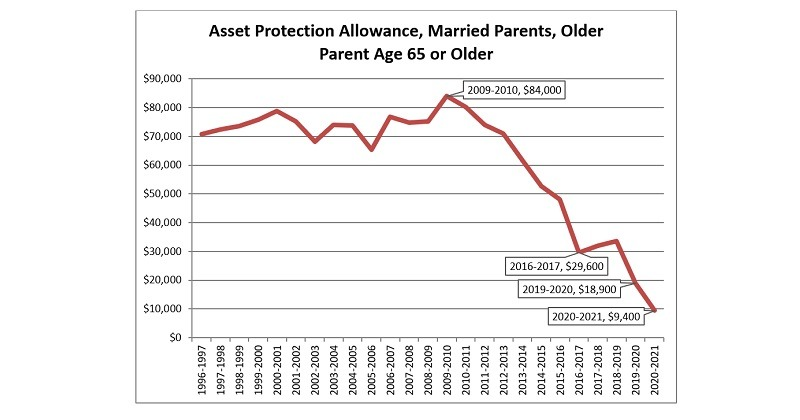

The Asset Protection Allowance is supposed to shelter some money from assessment to leave room for college savings, with the amount going up the closer the parents are to retirement. This number has plummeted since the mid-2000s, and it’s not something you can blame on the schools. I’m not sure who drove the changes, but they were not in families’ favor.

The asset protection allowance for a 65-year-old parent has decreased from $84,000 in 2009-2010 to $9,400 in 2020-2021. The $74,600 (88.8%) decrease is the equivalent of as much as a $4,207 cut in the student’s eligibility for need-based financial aid.

Age 48 is the median age of parents of college-age children. For these parents, the asset protection allowance has dropped from $52,400 in 2009-2010 to $6,000 in 2020-2021, a $46,400 decrease.

For a MARRIED parent. Single parents were always in the $10k range, at most. I had 2 kids going to college the same year and I think my asset protection that year was about $8k.

From the article you linked it says,

The asset protection allowance, which is based on the age of the older parent, is intended to cover the cost of an annuity which will supplement Social Security retirement benefits to the moderate family income level as determined by the Bureau of Labor Statistics (BLS). However, the average Social Security retirement benefit has been increasing while the moderate living standard has remained largely unchanged. As this gap narrows, it causes the asset protection allowance to decrease.

If they’re discussing the moderate living standard remaining the same, presumably because inflation was so low for so long, then perhaps the increase in inflation means that the asset protection allowance will increase?

Additionally (and admittedly, not my area of expertise), it seems a shame to have the asset protection allowance based on perceived Social Security retirement benefits when they are many employees who won’t be receiving any Social Security benefits (and thus might need more assets to make up for the difference).

Asset Protection Allowance Falls Short of Sheltering College Savings

The asset protection allowance was originally called the “Education Savings and Asset Protection Allowance” [20 USC 1087rr(d)]. But, the asset protection allowance is no longer sufficient to shelter the typical college savings plan for even a family with just one child.

Am I understanding the above quote correctly? That the Asset Protection Allowance is supposed to be both for covering living expenses between Social Security and moderate lifestyle AND to cover the remaining time in college (years 2-4, 3-4, 4)? And they think all of this comes down to less than $10k? I have to be missing something.

My concern is that it changed so wildly all at once without much discussion. Who sets the rules and decides what should be in the formula? Is there a process? I know they changed the rules pretty substantially again this year but I still don’t know much about the Star Chamber that produces the magic.

1 Like

The asset protect was used on FAFSA, which mainly controls Pell grants and subsidized loans. I don’t know that many students from families with $80k ‘protected’ in 2009 were Pell grant recipients, or that those who were suddenly became ineligible in 2020 because they had $20k or $30k in assets that were now considered in the EFC formula.

Some schools use FAFSA for their own calculations, but they can consider other factors (like assets tied up in retirement savings) if they want to.

Of course CSS schools do whatever they want and some may allow asset protection much much higher than $80k

1 Like