I took a peek at Firecalc, and am obviously not understanding it. First thing I did was to compare our yearly costs with their example (average yearly expenses for a couple with 70k income). Some of their statistics: Average property tax = $1300; Health Insurance = $817; Childcare/Personal Care=$214 I’ve tracked our own expenses for the last 25+ years, so know ours, but wanted to compare with other averages. Some of those numbers seem so far off, that I question the validity. Or we have some very high expenses while living in a modest COL area.

Those figures might work per month but they seem way off as yearly figures.

If the amounts shown are monthly, their yearly figures would be far off. Their total column = $27,146, including discretionary and basics. That appears far too low for monthly costs, and far too high for average yearly costs. That’s why I was curious what I’m missing here.

It’s based on income. I just tried it and the numbers are much higher than my expenses. The only line item that was in the ballpark for me was property taxes. Ignore the averages and use your own true expenses.

1 Like

Hmmmm. I guess that’s why I like Firecalc. I just use the calculator, plugging in my own information. I have never even seen anything suggesting what I should be using as inputs. This article explains how to use it: A Guide to FIRECalc: My Favorite Retirement Calculator - Four Pillar Freedom.

2 Likes

So, my mom has her retirement account managed by Vanguard. I took a look at it, and it looks like they have it all in bond funds (she has a separate account that has equities, so it’s not like it’s 100% in bond funds). I understand as you get older, there is less risk tolerance, however, aren’t bond funds now basically a guaranteed loss, with inflation and interest rates going up? I wonder if she would be better off if they just put the amount they would normally have in bond funds into a money market account.

She thinks she want to put it into what my dad’s account is, Vanguard Total Stock Market index, which has been a great fund. However, then she’s looking at putting all her investments in equities. She doesn’t actually need any of that money and may not access it for many years, if she ends up going to assisted living, as she still has income and assets. On one hand, I’m leery of telling her that it’s a good idea to have everything in equities, on the other, why keep it in money losing bond funds? Maybe some sort of low return stable index?

I would post your question on the Bogleheads website. People give excellent advice on that site.

10 Likes

I’ll do that kelsmom. Though I trust the people I know here, in particular.

For me, bonds are not necessarily for return, but safety from a market drop. So a small loss in ‘real’ rates is ok as they still provide safety. (That said, I keep my “bond” portfolio in Treasuries, which are slightly less volatile, allowing me to take the risk on the equity side of the AA).

If you mom doesn’t need the returns, there is as saying, ‘when you’ve won the game, why keep playing?’ In other words, no real need for any risk. OTOH, if she doesn’t need any set return, she could take more risk if she wanted to try to build something for her heirs/charities. But more importantly, the appropriate risk level is what allows her to sleep well at night.

5 Likes

I would say if she does not need a portion of her money for at least 5-10 years, she should invest that portion more aggressively.

2 Likes

I understand safety from a market drop, however, if it is “guaranteed market drop” when you could otherwise just have your money in cash with no market drop, maybe that’s the safer option. She doesn’t want to look at any of her accounts, they scare her, whether they are up or down. She’s afraid she’s going to touch the wrong button and do something illegal or make it all disappear.

I worked out the numbers, and this is what her net worth percentages are:

Cash equivalents: 30%

Bond funds: 12%

Equity funds: 38%

Home: 20%

She also has guaranteed income. Maybe switching the bond funds to equities isn’t that risky, as then it would be 50% of net worth. Of course, knowing my timing, the market would drop 30% the day after she switched over.

if you/she are concerned about a potential small loss in the small bond portion of the portfolio, why not more concern for a potential larger loss in the larger equity portion of her portfolio?

@bluebayou I’m not concerned about a potential small loss. I’m concerned about a guaranteed small loss. If it is clear that bond funds will be dragged down by inflation and interest rates, why stay in them when there is no upside potential? Equities go up and they go down, I feel quite certain that over time they will definitely go up, this is the long game. My mom could live for 25 more years.

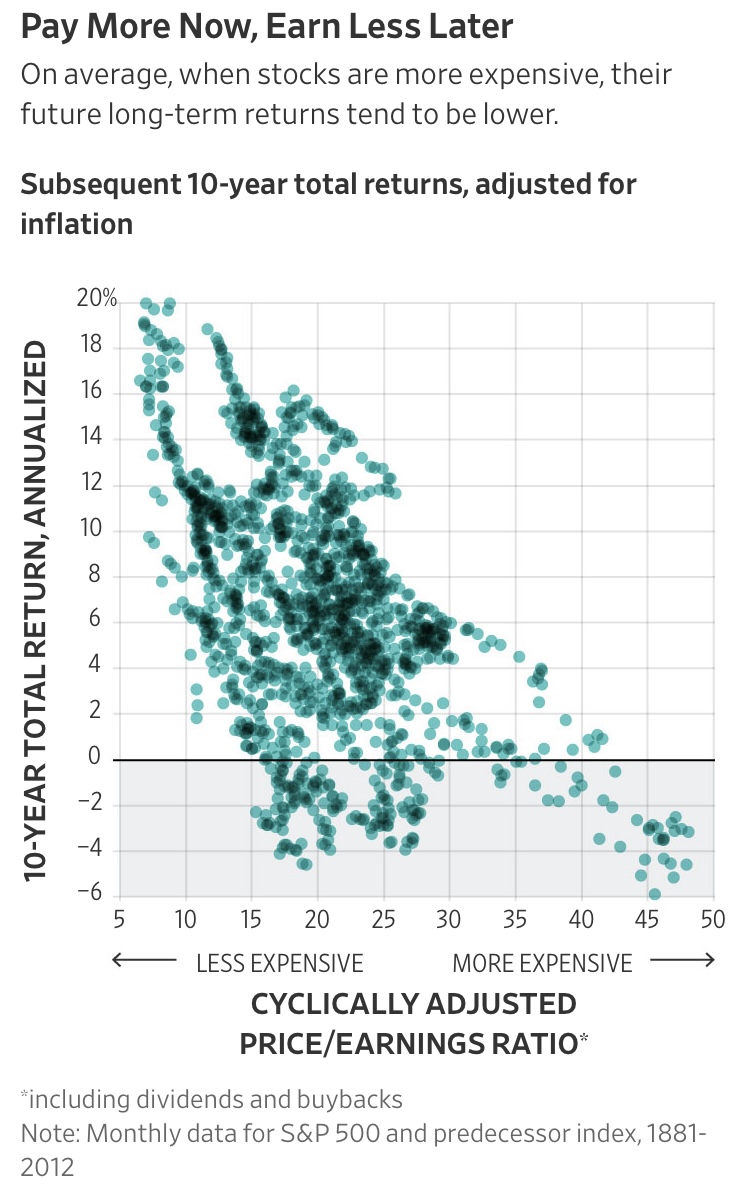

I found this WSJ article helpful in thinking about whether equities are “definitely” going up (note that current CAPE is 37.1, so in a range where historically the prospective 10 year returns have been negative about half the time over the last 140 years). To me the bigger question is whether this is money that is for all intents and purposes an inheritance, or something that might be needed in the future for long term care or similar.

1 Like

No telling what the funds will eventually go to. If she goes to assisted living and stays there for many years, she will access a great deal of it. However, with the cash on hand she has, it likely wouldn’t be for 10-15 years. If she doesn’t use it, it will go to inheritance/charities.

I feel responsible because I talked her into getting it managed by Vanguard last year. The funds have done well, except for the bond funds. Did I talk her into paying a 0.3% management fee for them to put her in a program that balances stocks/bonds, without looking at whether bond funds are a smart idea for anyone right now?

Is there anyone out there who is knowledgeable about bonds, who is keeping their bond funds going, even with the current inflation/interest rate situation? I understand that many just continue to stay the course, whatever happens, but what about those of you who closely follow what’s going on? Personally, I have some in a high quality corporate bond fund, that doesn’t have negative returns, but no other bond funds.

Individual bond prices change daily, but there is no loss if an individual bond held to maturity. Bond funds can lose money if the Manager has to sell some early. (Thus, many folks recommend bond ladders, i.e. a few bonds maturing every year or so, so there is no loss.)

That said, it seems to me that you are market timing on the bond portion but not on the equity portion of her AA, which is inconsistent. If you have a 25-year horizon for equities, why not a 25-year horizon for her bond funds? Or, are you assuming that interest rates will continue to increase for many years? (Again market timing, which is different than what the market sees right now.)

1 Like

Interest rates seem to have nowhere to go but up, and that’s what they’re doing. It hasn’t been much of an issue over the last several years because of the Fed, but now they are taking action. Market timing isn’t something I think she should do, with a caveat. If you are most certain that something is going to happen, I’m all for taking action. I can’t be the only one who thinks they have no idea where the stock market is going in the short term, but pretty sure the bond market is going down the toilet.

@busdriver11 we had a discussion with our financial advisor, which we were equally confused as this discussion is going as far as me understanding  .

.

We have someone who just manages the portfolio, which is different than our general contact and that’s who we talked to. We decided to change everything a little bit and be a bit more aggressive because of our tolerance for risk and our consistency of some of our income.

Was that a good idea? Who knows. But I guess I would see if she has a portfolio advisor and you, your mom and your siblings could discuss this with them.

But since my mother is equally nervous about everything anymore, if she is seeing gains in what she has now, maybe leave it be. And accept it for what it is.

2 Likes

@deb922 she does have an advisor, who we had a phone meeting with yesterday. And he forgot to write down on his schedule that he had a meeting with her, so now she has to reschedule. I’m concerned that these portfolio managers just put the formula in, it spits out a ratio, and that’s it.

My sister likely has no idea, she lets Vanguard manage her funds in the same way, hands off. I will ask her what she thinks, in case she has an opinion on that. I don’t want to say anything to my mom that scares her, I was happy that she allowed Vanguard to manage at all, as she’s had all her money in money market funds for decades. Good Lord!

The only reason I suggested meeting with your sibling is so no one can blame you later.

Yes, we have similar feelings about our advisor

3 Likes