My retired mother had some assets, but very low income (half my dad’s SS). The income was low enough that the IRS eventually sent letter telling her to stop filing.

2 Likes

Annuities are not inherently bad, but deferred annuities do provide the salesperson a commission. Even Bogleheads people recommend immediate annuities. If interest rates were better, I would be thinking about a deferred annuity. Whatever happens, I do plan to take a chunk of the cash category assets and annuitize it as we have no pension. Not sure how much, not sure how many different annuities, they usually have a benefit at $100k and above, but not beyond that, so a person might do multiples, at different companies, to spread any perceived company/product risk around.

They are not inherently bad but the products that are sold tend to a) be laden with hidden fees; and b)I pay big fees to salespeople. I wonder if you could get a much better annuity at TIAA. My interactions with them have been excellent, though with regard to annuities.

If a product has high margin, it can afford to pay salespersons higher commissions, which makes more of them selling the product. Guess where the higher margin comes from?

If you have a " need" for an annuity, first realize that a delay in collecting Social Security is your best and cheapest annuity available. Otherwise, purchase an annuity only from either Vanguard or TIAA, beginning at age 70. After that, ladder into them as you age, assuming your health remains good.

6 Likes

My brother (who earned a very strong salary/business co-owner for a number of years) is waiting until 70 because he likes the 8% he is promised with delaying his SS.

The cash flow for us makes sense. We used some 401k money to replace DH’s income (primary household income) from 2021 (he retired Nov 2020). I stopped working just before turning 65 and I began collecting SS Oct 2021.

Based on our financials, best to take SS now. DH is only making a little less per month than waiting (yes I know it affects him life long monthly) but our investments will be inherited by our DDs. SS should not be compared to an annuity - it is like a pension; when both spouses die it goes away. An annuity has a death benefit.

4 Likes

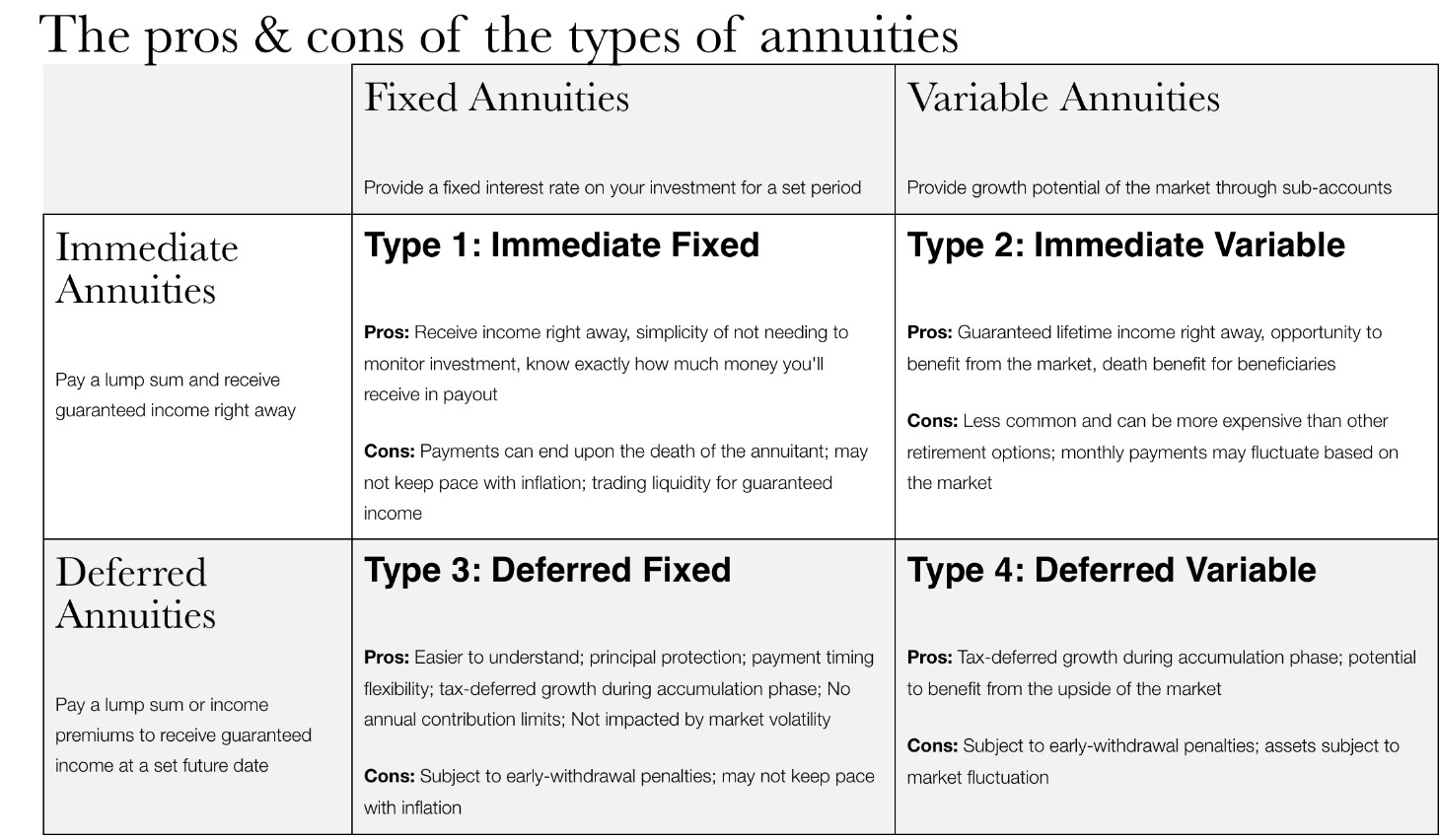

There are different types of annuities - Immediate/Deferred, Fixed/Variable. Description and pros&cons table here:

or 13 varieties in this article Understanding The 55 Types of Annuities (2023)

1 Like

Wanted to thank everyone for their input. I think I will make an appt with the Fiduciary my friend saw. See what she has to say regarding our situation.

As it stands, I devised a strategy for our SS and the FA we met with thought it was a good one. We have Traditional IRA’s, Roth IRA’s, currently have 3 homes. (Husband co-owns 2 with sister, one is rental property they plan to keep.) Husband will also get a small government pension, and has a TSP plan as well.

The guy we saw told DH that the Indexed Annuity will guarantee a minimum of 6% interest. It can go up, but will never go lower then that. We are going to meet with him again, where he will present us with the plan.

We can walk away, free and clear if we aren’t interested, or take the Annuity and his fee would be $600.

1 Like

With your situation, if you don’t have a tax advisor it may be worthwhile.

Our Fiduciary FA has his own tax person, and so he directs a lot of questions to his tax person. DH and I are ‘uncomplicated’ but we still are gaining by keeping taxes in mind with decisions. Our Fiduciary FA has been terrific for us.

1 Like

I know we need to do a lot of evaluating and research. I like to research as much as possible where DH tends to sign on way to fast for my liking.

This is a long established family firm. They have someone who is familiar with DoD employees/retirement, which is great, as it has it’s own complexities, and they also have a tax preparer.

I would be more likely to go elsewhere for the Tax Advisor. Although now, with tax season, will probably have to wait a bit.

Will schedule with the Fiduciary for a second look.

2 Likes

The Roth Rollout (Conversion) strategy has us converting some level amounts of retirement funds (most likely from our 401k which is sizable) to our Roth IRA to get our tax projections pretty close to the same as when we need to take RMDs. We save on tax expenses in the long run (we will be paying the extra tax on these years with the conversions but are at our same low level tax bracket, but less taxes when we need to take RMDs since we had some of the funds converted into Roth IRA). It also adds value to our estate.

Retirement is a ‘juggling act’ for sure.

Now to figure out state and federal taxes for this year and have appropriate funds in place there. This past year we overpaid in Federal because the money we took out of 401k which automatically had 20% withholding for Federal Taxes. However we needed to pay state taxes, but actually had a very tiny penalty. Our current income stream has 10% Federal tax withholding. So now I need to see if 10% is enough; I know what our state obligation will be and plan to have that taken care of.

@laralei, may have missed this, but do the annuities you are looking at have any form of protection against inflation? This could be important if we are in a higher inflation environment for a while.

I would love to convert to Roths, but have not hit a point where it makes economic sense. The balance would be tipped a little bit if I moved to a state with no income tax. A very significant part of my retirement savings is in 401ks (and a little bit in a TIAA-CREF account from when I was a professor early on in my career). Both could be rolled into IRAs and then into Roths if I were to stop making money.

1 Like

And it all depends on one’s age. We have time between now (age 65, both retired) and 72 RMDs.

When one is making very good money and enjoying their work, they have to ‘give up’ certain tax breaks us ‘less financially worthy’ people get.

As it sits now, DH/my estate has surpassed my parents in current monetary value, but not if you adjust for what the money in 2011 would be worth now. However we have just 2 children/3 grandchildren, while parents’ estate got split by 5 children (and two small life insurance policies got split between the 8 grandchildren.)

Our DD1/SIL/GKids are going to be moving to TX. SIL will go first. DH and I are going to be a lot of help to them. DH helped drive a Penske truck for DD2, and will do so with the family move (late Nov). I think DD2 and DH will drive with a UHaul late Oct to scout for a rental for the family (SIL is in training not where they will live) and rent a storage unit for the U-Haul stuff that will be close to where they will live. I will babysit the kids and continue with their M - F schedule at FT child care where they currently live. What may not fit in Penske truck can be in a U-Haul with the family drive (DD2and 3 kids). They can hire loading help in their city just like DH/DD2 did at DD2’s move to FL. Have not figured out details like if I should also drive to TX and then DH can return with me - which probably should happen so both of us can help them get settled. Don’t know how much time SIL will have before he starts work (50 hours/week job with 10 hours/week OT). We have some family members in TX (DH has relatives as do I, as does SIL) but depending on where SIL is assigned…

I also have some friend networks in TX - friends from growing up/HS, friends from my time at TAMU and our work times in TX, and friends that are with another college network. Always nice to reconnect with friends if we are anywhere near where they currently live.

2022 just got ‘busier’ for DH and me. Early in married life DH and I moved 5 X in 6 years across 3 non-connecting states. Since then we only have had local moves. In early years we had not much stuff and had company paid moves for 3 of the moves (2 across states and 1 with company transfer that was more than 100 miles away, but barely - Houston to College Station TX).

1 Like

Agreed @SOSConcern. I’m 67 and ShawWife is 65 but both of us are working because we love what we do. In principle, we could retire but neither of us can think of other things we’d like to spend time on. I’m trying to reorganize my business to reduce or eliminate my dealings with one highly talented and highly annoying colleague. Life’s too short to mess with that. And, I’m increasing the amount of time I spend on pro bono kinds of projects.

ShawWife is probably hitting her stride professionally and her work is also her therapy – she jokes that we would probably be funding therapy if it weren’t working.

It does sound like your H is getting into the moving business post-retirement in addition to you taking care of grandkids for a while. Enjoy networking with friends.

3 Likes

Retirees are going back to work mostly due to worries about stock market uncertainties, inflation… even Tom Brady is coming out of retirement… you’d think he saved enough, but guess not. ![]()

https://money.yahoo.com/older-americans-head-back-to-the-workforce-171922301.html

3 Likes

Does anyone wonder if writers have an opinion and they find the evidence to support that.

It seems to me that we have only been worried about inflation and the stock market for a short period of time.

To me, maybe it’s also that the public perception of the pandemic is that it’s waning. People are getting back to the office, schools are becoming where they aren’t closing. People feel more comfortable working. And maybe older adults retired to watch grandchildren and now those daycare options are opening up also.

Sometimes I get frustrated that there are these articles that seem as if the conclusions are decided before it’s written.

8 Likes

Very interesting. In our circle, tradesmen, blue collar, no working from home during pandemic, everyone is planning their retirements.

My SIL works in accounting office of large hospital. They’ve lost several personnel to early retirement. She is 62 and would leave tomorrow, but can’t afford to.

Her former BF is selling off all his rental properties, he’s done at 64.

Out for breakfast recently, and one of the guys in another booth expressed how he can’t wait to retire. He is in construction, and he is out at 62.

Another table, said he had a year and a half, and my DH contributed Dec 31, 2024! At 63.

Maybe not “college educated” but certainly not unskilled labor either. Wonder how many of the younger generation are going into the trades to replace them?

3 Likes

My personal anecdote about youngsters going into trades: recently, the roofer who installed our metal roof, the plumber who did some water main work, and the mechanic who serviced our boiler all showed up with apprentices in tow.

9 Likes

My husband just retired. He’s doesn’t seem to be worried about either inflation or the stock market. It doesn’t feel like that narrative was a narrative before he retired on January 1. We’ve barely figured out how much we are spending let alone think about going back to work. Our investments had a great 2021, 2022 has barely started.

And I agree, so many are thinking of retirement now. My husband was a manager but he had many in skilled trades. They are hard, physically demanding jobs and people are tired. I know the kids here who go into the skilled trades are finding good paying jobs. Sometimes I think that if we have white collar jobs and our kids are going to college, then we don’t see the kids who want to find a skilled trade. But maybe they are hard to find kids who want to do them. I’m not sure.

I hope I’m explaining myself. Sometimes I feel that I can’t express what I want to say ![]()

3 Likes

Tom Brady and his wife spend money like they have Saudi assets. I saw a while back in Forbes where they bought property where everyone else was Uber wealthy. Maybe he will spend less if he is working, ha ha. Maybe he also missed the excitement he got from playing.

DH and I have no regrets retiring when we did. Have the time to help our kids with things like moving, and have no excuses for not having a fitness regime. Schedule is happily clear. We also don’t need to spend a lot in retirement to be happy. I will travel a bit, but DH is happy to be a home body after a lot of business travel he could do without. However he often traveled with people that wanted to see stuff so he also saw stuff.