Yeah, I read through the fine print. It’s just a promotional rate for six months, then they think they’ve sucked you in to their mega rate. Ha, little do they know, we will not get sucked in!

3 Likes

Yeah @richenough, we have the same problem. Even in years that seem like bad years, I make too much for a Roth conversion to make sense. Which, I guess, is a good problem. But I look at it periodically and it has never worked. I now have a pretty large 401k, but will be paying taxes out the wazoo unless I stop working and am able to convert. And, I’m not planning to stop working because I like what I do (and I also like the money).

3 Likes

Whenever I get an unavoidable tax hit that I didn’t anticipate my mantra is “I still have more money than I started with”.

10 Likes

@notrichenough and @shawbridge - it is wonderful that you enjoy doing what you are doing, and enjoy the financial benefits. You can see when you will need to pay more taxes or do some spend down when the time comes – and it may be that philanthropic endeavors can help. You have time to think about ‘best use’.

IMHO we are in the ‘comfortable enough’ category (although can always have a point that if one of us needed very long term care, that goes through resources quickly). DDs have big hearts, and DD1 is BSN - so if/when the time comes - we may be dependent on them to be the ‘parents caring for parents’ with using up our resources in best manner for our end of life needs.

DH and I are both 66. Last year we converted $25,000 from 401k to Roth IRA, and also had $5,000 out of 401k to IRS. We just did the same this year. Always have to think about tax consequences, and structuring what we want to do things and how to go about doing what we want to do in the best way possible – timing and direction.

Interestingly, DH’s former college roommate, who a few years ago said he planned to work more years (able to work from home, and at that time enjoyed the work) - well now he also has retired. Between grandkids and more medical appointments, and maybe more demands at the job…DH’s best friend from growing up - as soon as he retired last year, his wife had a whole travel agenda for them to fulfill (Australia/New Zealand, Peru, etc.) and have been going on big trips ever since (their kids are the same ages as ours - 27 and 29, and both of their kids are single and doing well in their careers, live close to parents).

I am thinking more of our next generations on use of much of our extra financial resources - staying close to home this year except for travel to or with family (we have a family wedding in April, and relocation of DD1/SIL/Kids). DD1 (who just turned 29) is expecting baby #4 in June (her DH is 33 and had a late start on his career). DD2 (turns 27 this month) is in good career job in location that will be where she stays (and loves it there) - her long time BF (26) is having to move around in his sports management career, so eventually he will land where she is.

I have a friend that just ‘retired’ from being a HS English teacher - met the years in along with age for full teacher retirement. Her DH is continuing to work FT in his current job. She just got another job, which is such a great fit for lifestyle, and she works 16 hours/week.

Expect to be in our current home maybe another 10 years - unless circumstances have us move. DH is very involved in some things here that won’t be replicated elsewhere - so when he is ready to ‘move on’.

I have a friend making a big move (she and DH are both retired) - and I know how much work that is – she has very structured days to get everything done.

I think it’s @notrichenough who has been posting on this thread!

1 Like

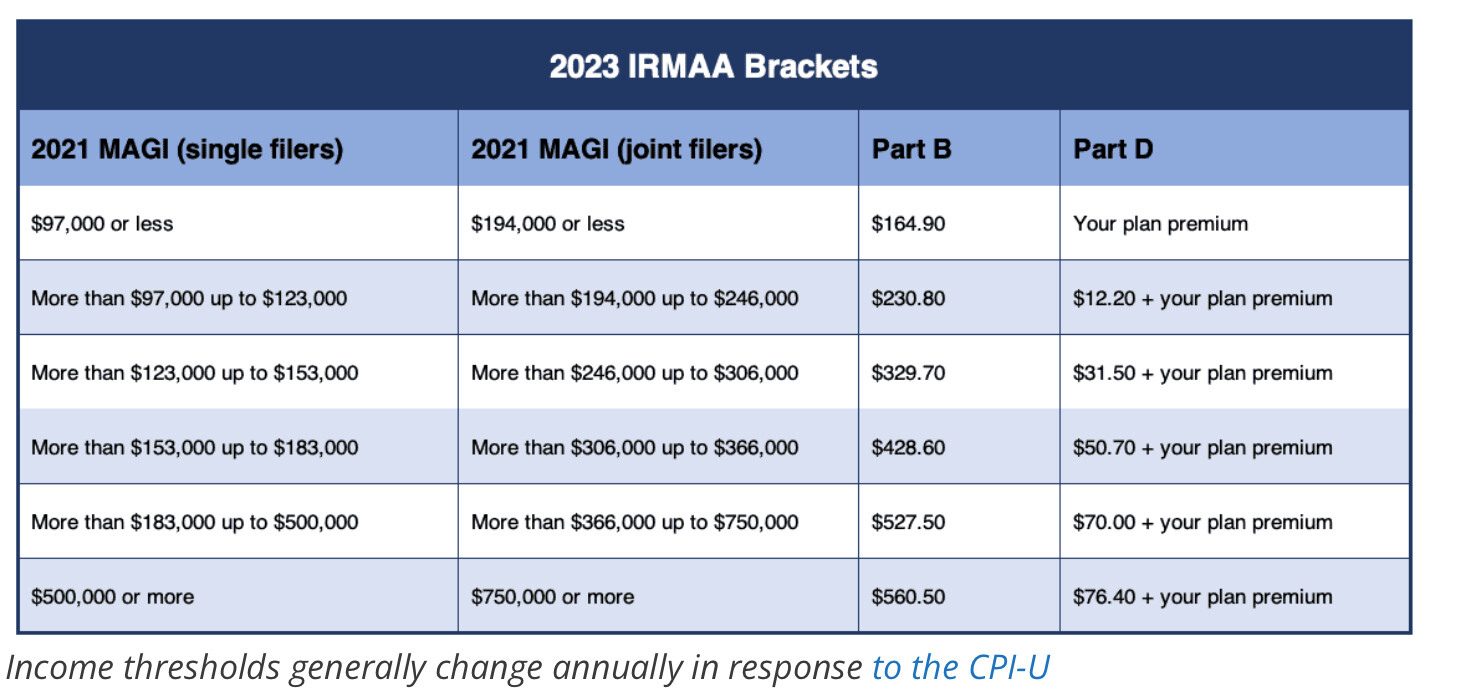

With very large income (RMD + other taxable income sources), those extra taxes possibly could include extra medicare costs…. IRMAA (x2 if married).

From The 2024 IRMAA Brackets – Social Security Intelligence

Most retirees won’t have enough income for IIRMA concerns. I posted the chart because IRMAA is a factor for those considering Roth rollover. Need to be careful about doing big chunks of Roth conversion, especially at age 63+ (IRMAA is based on prior income).

5 Likes

I think I already have IRMAA, if I’m not mistaken. I wonder if a Roth rollover would make it meaningfully worse.

1 Like

The buck stops at 1/2 mil for single filers and 3/4 for joint. ![]()

1 Like

We pay an IRMMA already. It went down this year…and will go down next year also. Then it will stabilize.

I’m happy to be making my charitable contributions from an IRA I have. I am already exceeding my RMD and I’m not yet 72. But soon! This will come out of my IRA until DH reaches the age where he needs to do RMD…and then we will switch to one of his accounts.

I wish I could make my kids into a charity🤣

4 Likes

For those of you new to retirement planning, RMD is “Required Minimum Withdrawal”…. the amount you must annually disburse from traditional (taxable, non-Roth) IRA starting around age 72-ish. RMD start age has been creeping up recently, so I’m not sure this calculator link is current… but it gives you the jist (starts around 4% and increases over time).

Note: There are many tables available online to show “factor” (divide IRA balance by that amount). For example: if factor=25, RMD = 4% (thus a 100K IRA would have RMD of $4000). Hubby and I roll our eyes because we’d rather see a table of percentages, the inverse of factor.

4 Likes

I swear, the government seems to enjoy making it difficult to understand these things … just at the point in many lives when understanding difficult concepts is even harder than it once was.

6 Likes

Sometimes my husband and I roll our eyes on taxes/whatever, feeling stupid and comment “I wonder how the more stupid people deal with this”.

4 Likes

On the other hand, it’s shocking how many intelligent, well-educated people couldn’t figure out percentages if their lives depended on it.

Including my wife, sad to say.

That surprises me. But I’m an engineer and have mostly been with techie folks (Including hubby. And our kids, who once helped their babysitter with her math homework). Your wife likely has other expertise and wisdom that we lack.

2 Likes

Honestly, sometimes various IRS codes are written with lingo and the kind of thinking that is instilled with government policy/procedure. Sometimes one may have to learn or know the basis of the original tax law and then how it changed. Sometimes that is also about ‘finding’ various ways around the applicable rules.

It also is evident with how SSA and Medicare has been set up, and then patches of changes. Sometimes they don’t make some important things obvious to find, or they don’t spell out what rules supercede others unless you know where to go look, or have learned a lesson on this.

H & R Block has a special software for military (and use is free for active duty) – DD uses it, and it lays out the types of commonly used exemptions and tax deductions or tax credits. She also has used it as a VA employee - IDK if she had to pay a small fee to use it or it was a VA benefit.

Many of us use Turbo Tax unless we know we have a more complicated tax year or tax circumstances.

We have a local property tax ‘senior rate’ - when a person on the deed is 65 - but you have to specifically go to the tax office and show your driver’s license or State ID. Then it is good from the next year moving on. They are quiet about it - you have to know or specifically ask. I had seen info on the low income and disabled discounted property tax, but I had to specifically call and ask. We missed it for the first year we were eligible; our house was assessed based on a new home mortgage, and I just thought I would call, ask, and be sure.

Talked to someone today who purchased a home from an elderly woman, and she had been paying the full property tax rate for 10 years when she could have paid the lower rate (1/2 plus $50). The new owners had to split the property taxes, and that is when the realtor discovered how much this lady had been overpaying on these taxes.

That is how certain laws work. You find out about it and just have to suck up your lack of being informed.

3 Likes

I had a really hard time understanding non deductible IRA basis, reporting conversions and tracking Roth conversions & rollovers. I did not find TurboTax to be intuitive in this regard, either. I actually just finished amending form 8606 for three years to get reporting on track. And I am really good at interpreting regulations. I’m honestly happy to have a financial advisor to help with withholding taxes on IRA withdrawals, figuring out how much to convert to Roth each year, and (someday) tell us how much our RMDs are each year.

1 Like

@SOSConcern wrote - “Honestly, sometimes various IRS codes are written with lingo and the kind of thinking that is instilled with government policy/procedure. Sometimes one may have to learn or know the basis of the original tax law and then how it changed. Sometimes that is also about ‘finding’ various ways around the applicable rules.

It also is evident with how SSA and Medicare has been set up, and then patches of changes. Sometimes they don’t make some important things obvious to find, or they don’t spell out what rules supercede others unless you know where to go look, or have learned a lesson on this.”

What a great observation! Years ago we did our taxes ourselves, but have used an accountant for many years now. Recently I tried helping a friend with their taxes and quickly learned that the formulas on Schedule C, the Self Employment form, and the self employed 20% exclusion form were headache inducing. Now, I’m beginning to understand that what @SOSConcern calls “patches” are the source of my exasperation.

@kelsmom - In order to avoid the RMD problem, we’re slowly but surely converting our traditional IRA’s to Roth’s. We’re already over 90% of the way there, and should complete our conversions within a few years.

4 Likes

After posting above about converting out traditional IRA’s to Roth’s, I realized that my wife will face RMD’s on a 401(k).

Can this be rolled over into an IRA and then converted to a Roth?

The 401(k) and the IRAs are all considered with the RMD type of funds. Moving from 401k into IRA - it depends on the 401k plan rules as can be clarified by administrators/administration IMHO. Can she call and see what her options are?

The way DD moved her state pension type funds was to go to IRA and then into Roth IRA. She had a TD Ameritrade Roth IRA account, so TD Ameritrade set up a temporary IRA account first.

@sherpa here are some things to consider when deciding to roll over or not.

3 Likes