My point is there are instruments that have much lower risk and it’s liquid. Seriously, there’s hardly anything that doesn’t have its own risk. Using your credit card has risks, driving has risks, getting up in the morning has risks…

Yes, nearly everything has some risks. My point is that investors (and savers) need to understand when there’re extra risks so they know where the extra yield may be coming from and can compare accordingly.

+1 to this. I am so thankful my parents never made us promise not to put them in a “home”. My mother had Alzheimer’s and assisted living was the best situation for her. MIL is now in an assisted living (it is not safe for her to be at her own house unless she had 24/7 care).

Thankfully they both could/can afford this.

8 Likes

We are hopeful that we won’t have to ask our kids for help as we age. I guess you never know for sure, but we believe we will be able to handle most scenarios ourselves, without relying on at least finances from the kids. Of course we can’t control the emotional burden.

3 Likes

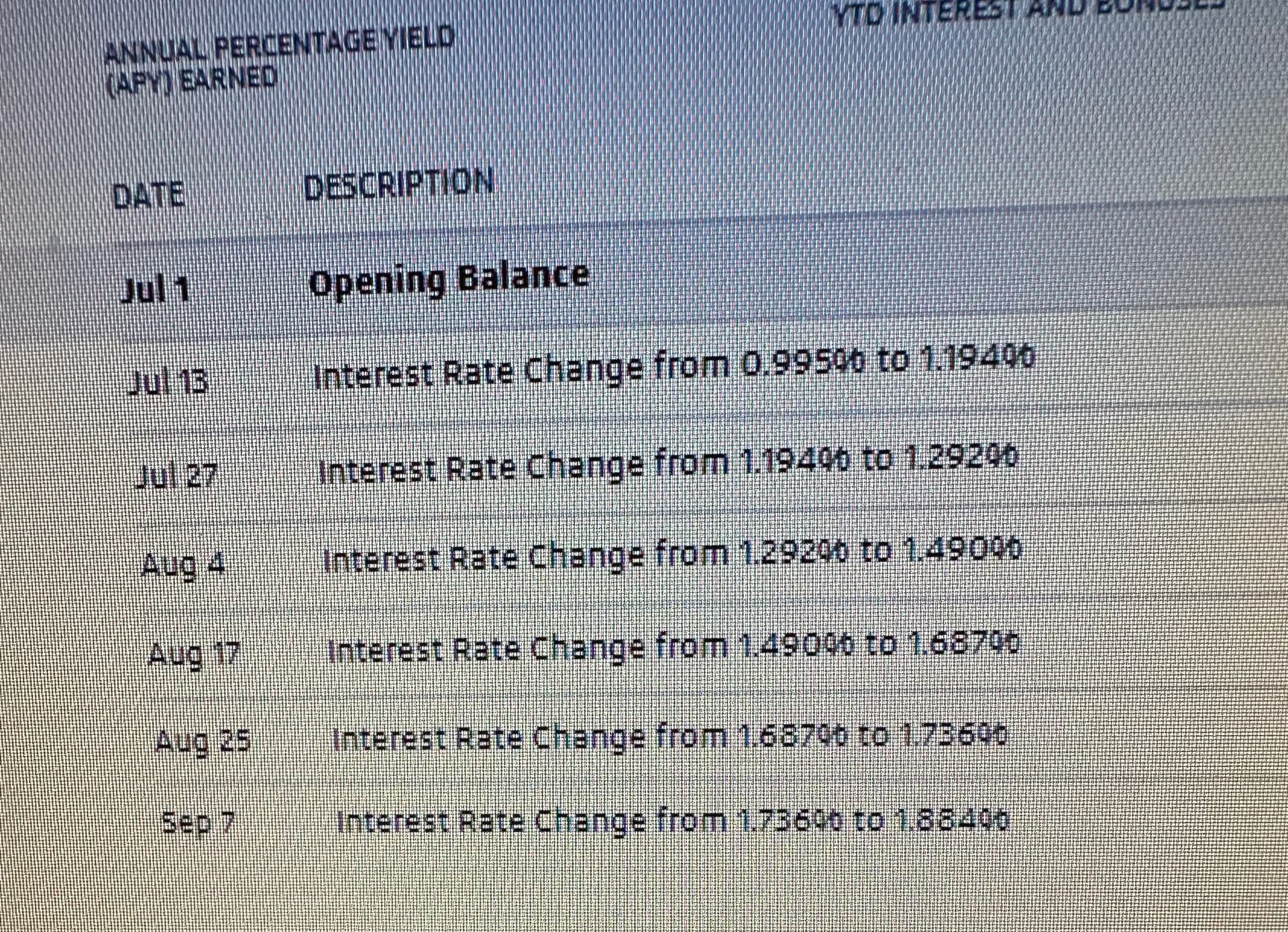

I have a savings account with Discover bank. The interest rate just went up to 3.6 percent. Zero risk (FDIC insured) and I got a bonus for opening the account and leaving it there for three (I think) months.

1 Like

Morgan Stanley’s preferred savings account has been at 4% for the last 6 or more months, and I expect they’re ready for an uptick.

I never thought I’d see the day again when savings account returns were at least interesting, if not compelling. Insured 4% return … could do a lot worse.

3 Likes

Moved most of our USAA savings to 1) I Bonds (6+%), 2) Vanguard Money Market (4.5%) and 3) 52 week T-Bills. USAA was still paying .01 percent, which was just ridiculous.

H changed his TSP 401k to laddered target funds in late 2019. We have them staggered over 2030,2035 and 2040. It helped blunt the crazy market ride since.

My IRA is still 70/30 (I’m 62). We won’t be tapping it til RMDs.

3 Likes

I used to have a savings account with Discover, but now that interest rate is more relevant I favor other alternatives with higher rates. These include:

- T-bills from prior to last week’s banking issues, when 17-week was >5%

- No-penalty CD (can withdraw early while keeping all interest payouts, interest compounded daily) at 4.75%

- Money market at ~4.5%

Which no penalty CDs did you buy?

This 4.75% no penalty CD was added in response to the SVB collapse. Many other banks also improved CD terms shortly after the SVB debacle.

2 Likes

I had an online savings with capital one 360. Interest rate plummeted and I pulled the $

What’s the difference between a no-penalty CD and a regular back account?

Capitol One 360 plummeted? Currently 3.4% . Was it higher?

You can’t do standard banking transactions with the referenced no penalty CD, like you could with a bank account. You only have the option to keep the full balance in the CD or withdraw the full balance from the CD. If you choose to withdraw, you keep all interest payments, which are compounded daily.

I had Cap 1 “high” yield saving account, but they changed it to about nothing, and created another type of account. I FINALLY put a bunch in the new account, and at 1 point at least it was close to 4%. I’ve banked with them “forever,” but they do have some stinky ways of handling things.

2 Likes

Their savings account interest dropped to a pittance- pulled the $ and didnt look back

1 Like

Are you worried about the exposure Ally has in the auto finance market? I am hearing that might well be a pretty ugly affair with defaults ratcheting up.

By a variety of measures Ally may be in worse financial shape than typical US banks. I expect this contributes to why Ally offers better CD rates/terms than typical banks. However, I personally feel that the risk of a SVB like failure prior to CD maturity is extremely low. The market seems to have a similar opinion. Ally stock has had the same ~20% drop in past month as Wells Fargo, Bank of America, and similar. This is a much smaller loss than First Republic stock, which has dropped 90% over the past month. That said, I don’t intend to put more than $250k in Ally.

1 Like

How do you set up a trust to avoid drawing assets? Isn’t the trust included in a person’s asset and gets depleted if needed?

1 Like