My husband has been watching Fast Money and Jim Cramer for about 3 years and now is doing stock picking with a buddy who has some finanancial investment experience.

I put on my headphones when Mad Money comes on CNBC and try to stay non-judgmental. But SO agree with the comments upthread - how does one think that the market can be outplayed (as a neophyte layperson) when there are people with 30 years experience, advanced finance degrees, and loads of inside track info playing it?

The friends I know who mention stock-pick methods do it as a hobby (one as part of an investment/socializing club), with small money they could afford to loose. Perhaps others do and don’t talk about it, but I get the sense that they, like us, are mostly in index funds.

I mean I’ll admit I do stock pick for my own portfolio although I have to clear every single trade which becomes a real nuisance as I could be stuck in a position if my firm is also selling the position. But I believe the market isn’t even weak-form efficient and therefore stock picking is logically consistent with my beliefs.

I mainly run a core-satelite model where the core is invested in an index and the rest I individually stock pick + buy e-minis/gamble.

As mentioned above though, I definitely don’t think investing in individual securities makes any sense.

Does he use the “inverse-Cramer” portfolio (shorting anything he recommends)? That seems to have been quite successful lately, given Cramer’s recommendations of companies like First Republic.

Edit: apparently the strategy gave stellar returns in 2022 but the more bullish market over the last couple of months has not been so good:

The main reason people should pay financial advisor fees is advice. If your advisor is just managing assets, I personally dont think it’s worth it.

Good advisors should have working knowledge of core financial planning principles including tax strategies, social security, medicare, risk protection and estate planning.

Nothing wrong with active management either - I would do all sorts of things to be allowed to invest in Citadel’s Wellington Fund (they’re not open to investors like myself).

Their returns are absolutely legendary - they even returned 38% in 2022 while equity markets absolutely crashed + bonds became positively correlated.

A $10,000 investment in 1990 in the Wellington Fund would have returned $1.3 million by 2018.

Are you considering losses to fees? The fee structure doesn’t appear to be public, but one article mentions 5-10% per year + 20% performance fee on profits, quoting an anonymous source. The fees seem high enough to have a notable impact on overall return for an investor.

One also needs to consider survivorship bias influencing past performance being an accurate prediction of future success. The large portion of funds that don’t perform well often don’t last. I’m not saying this particular fund’s success was due to random chance, but in a hypothetical situation where degree of success is primarily due to random chance, a few funds are going to randomly be multiple SDs beyond the mean for their risk level. When looking at these successful funds, it can be difficult to identify what portion of past return is due to luck and what portion of return is likely to continue in the future.

For example, I ran a search for the best performing hedge fund over a multi-year period in 2010. By far the biggest winner was Paulson Credit Opportunities . Nobody else even came close. The fund did especially well in the subprime mortgage crisis and recession. When most were losing in a challenging market, they made large gains. It’s been frequently compared to the one you mentioned for a variety of reasons including the 2 funds have the 2 highest single year gains as measured in billions of assets. The fund’s performance was also described as “legendary” in articles, Investors flocked to the fund. It 2007 alone, the Paulson’s managed assets increased from 6B to 28B and 36B a short time later, making it the 3rd largest hedge fund in the world by managed capital. However, the legendary success didn’t continue long with huge losses shortly after 2010, and a subpar long term return overall subsequent decade. As such, Paulson’s managed capital dropped rapidly to a small fraction of past levels, back down to pre-2007 levels of 6B. A few years ago, Paulson made the decision to return the remaining hedge fund capital back to investors and convert to a family office, as many of his peers have done.

Are you considering losses to fees? The fee structure doesn’t appear to be public, but one article mentions 5-10% per year + 20% performance fee on profits, quoting an anonymous source. The fees seem high enough to have a notable impact on overall return for an investor.

Yes, I’m considering fees. According to the FT, Citadel’s fund has driven returns of 19.1% per year since inception in 1990. Fees are extraordinarily high from what I’ve heard but the returns more than make up for it.

Citadel’s flagship multi-strategy Wellington fund has delivered annualised returns (after fees) of 19.1 per cent since its inception in 1990, according to information provided to the Financial Times by an investor in the hedge fund. Citadel declined to provide performance data for this article.

And as to your point about survivorship bias, there absolutely is survivorship bias. But I certainly do not claim that hedgefunds outperform the market as a whole nor will I say for certain that it wasn’t down to luck.

But to outperform over a 30 year period is very, very unlikely unless the fund was adding value in some way.

When looking at these successful funds, it can be difficult to identify what portion of past return is due to luck and what portion of return is likely to continue in the future.

Sure. And it doesn’t help that data for most funds is very secretive which adds to survivorship bias if you’re looking at any sort of index composed of hedgefunds.

If it were easy to allocate capital, fund-of-funds wouldn’t exist.

And it’s certainly possible that Citadel’s Wellington Fund could blow up. There’s no guarantee - it was just my opinion that their track record is legendary.

Those that “dabble” in alternatives, would you speculate and buy a 3X leveraged bull index ETF and hold? If the annualized return is something like 8% per year over 10 years, would it make sense to do this and hope for the best?

I don’t frequent bogglehead forums. That would be completely against the philosophy of boggleheading. Lol.

But, what is the TLDR? In any event, I am going to do this after June 1 and see what happens.

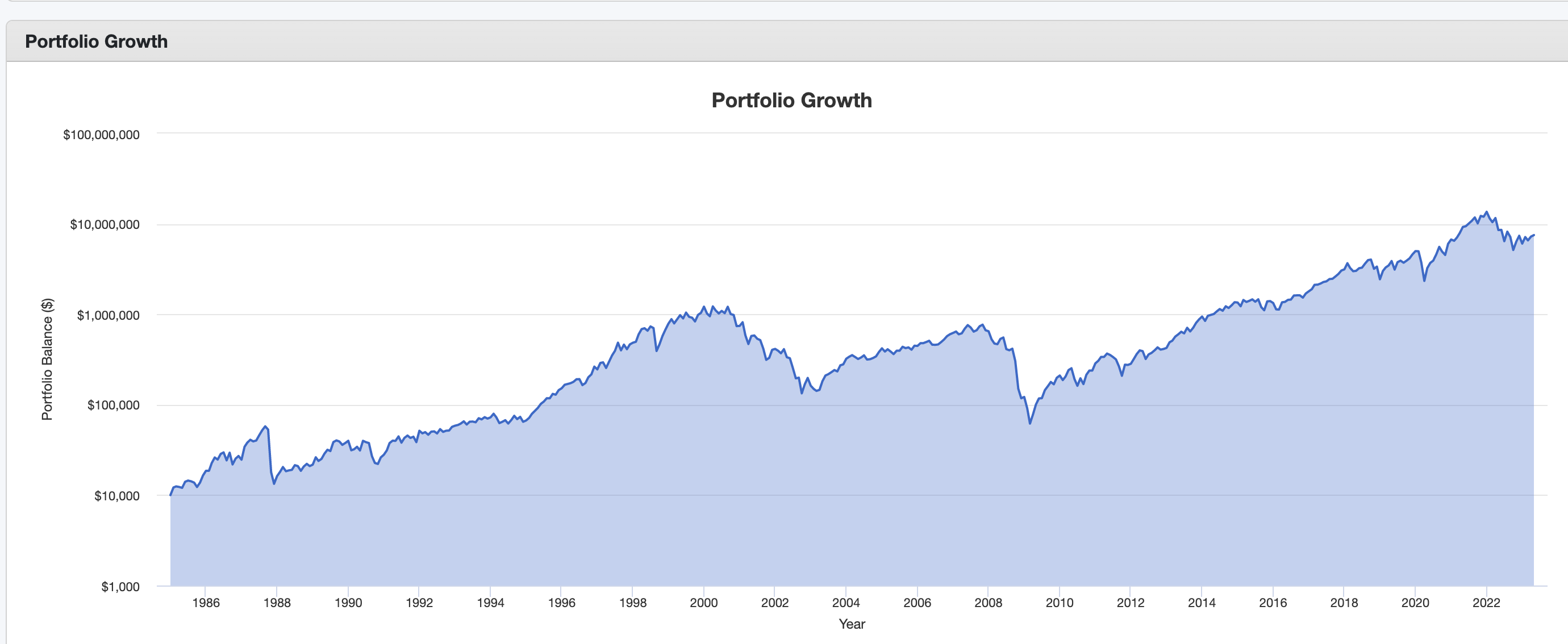

I ran a backtest for you from 1984 to 2023 if you held a leveraged security. Note that I was lazy and I didn’t really bother to change interest rates or simulate actual returns so returns will be slightly/very exaggerated.

@1dadinNC, I have invested in alternatives (a hedge fund that I helped start and then two Carlyle PE funds). I have done very well in the first two. The third one is newer – have not yet invested my full commitment – and have not received any distributions.

I would not invest in a leveraged ETF. Does not cut downside volatility. I’m either looking for an edge (the hedge fund identified a kind of trade that worked well for several years and then faded away over time and we shut the fund as we no longer had an edge) or superior deal flow/skill (what I’m looking for from Carlyle). I would look for returns that are not highly correlated with the S&P 500 but that have lower downside volatility.

I’m back to debating whether to start drawing my pension. We don’t NEED the money so I think why touch it. If I wait four more years, the monthly amount will max out so I’m inclined to wait, but wait for what? Anyway, here’s my new question …

If I don’t touch it and get hit by a bus tomorrow, dh gets the benefit.

If I start it and elect to not do a joint and survivor option, then when I get hit by a bus the next day he gets nothing.

Of course, I could do a survivor benefit option, but he doesn’t need it so we are leaning against that. He has his own pension and SS and will get my 401k.

The question: Are there some factors I’m missing when making the decision about whether to do a joint and survivor annuity? TIA FYI, this isn’t a huge monthly sum, but it’s enough that I don’t want to screw it up!

ETA: We are 60, and our parents lived until late 80s (his) or early 90s (mine).