We live in a low property tax state, and our state taxes are low (AL). Also, in our area, you file with tax assessor when you turn 65, and our property tax is 1/2 plus $50.

However at some future time, we will be selling our house to relocate - but not quite sure where to at that point. I don’t want to downsize to move and stay here. Moving and selling property is a big task. There are some home improvements I want to do to have our home sell at the price it can be with updates.

DH is active with things here, and we will find out in the next few years if DD1/family will be staying where they moved to (TX) - and in the mean time, I will have some travel via airline to them and scope things out. Maybe have a condo there (2nd residence). We have family and friends in that state too, as DH and I lived there right out of college in two cities over 5 years before we have been in our area since 1983. We are use to our state, but DD2 lives in Orlando, and we will need to decide if we want to learn FL and make the adjustment to going there for primary residence. DH isn’t keen on FL, so time will tell what he will feel like when the time comes for him to want to wrap up things here.

Controlling expenses and still living well.

One has to weigh out where one wants to live. One can live in more expensive place with modifying lifestyle, and often one is motivated and happy to be living there for a variety of reasons.

One hears about the other two reasons for a special classification on property assessment, one is for low income, and the other is for disability. I missed the tax break for 1 year - I just happened to check when we refinanced our home. A good friend missed this for several years, and they actively were buying and selling properties. Another friend bought a home from a senior, and the senior citizen overpaid property taxes over 10 + years.

Can’t rely on real estate agents to tell about this. One has to show ID to tax assessor office, and they log it into their system. Have to do it prior to a certain calendar date for following year. We get a tax bill in Oct and is due by end of the year, and this is our first year for getting this tax break.

They raised ‘fair market value’ on our property, and they have been gradually doing this year by year on everyone - we are in a relatively high growth area. Since I had an appraisal with refinancing, I got the tax assessor’s office to reduce their fair market value number when I emailed in my property appraisal - they came back within 24 hours with an fair market value just below our appraisal. (reduced the value by $30,300 from what they originally mailed me). Last year’s fair market value was $50,700 less than the jump they had for this year.

So I will see the tax due in the billing statement in October.

Had I visited the tax assessor office in the prior year when we were eligible for the special classification, it would have saved us over $ 1,300.

As I said, we have generally low property taxes.

I have a friend who moved from CA to Arkansas, with significant COL savings. Has a beautiful lake property. Greatly reduced expenses while maintaining a similar life style.

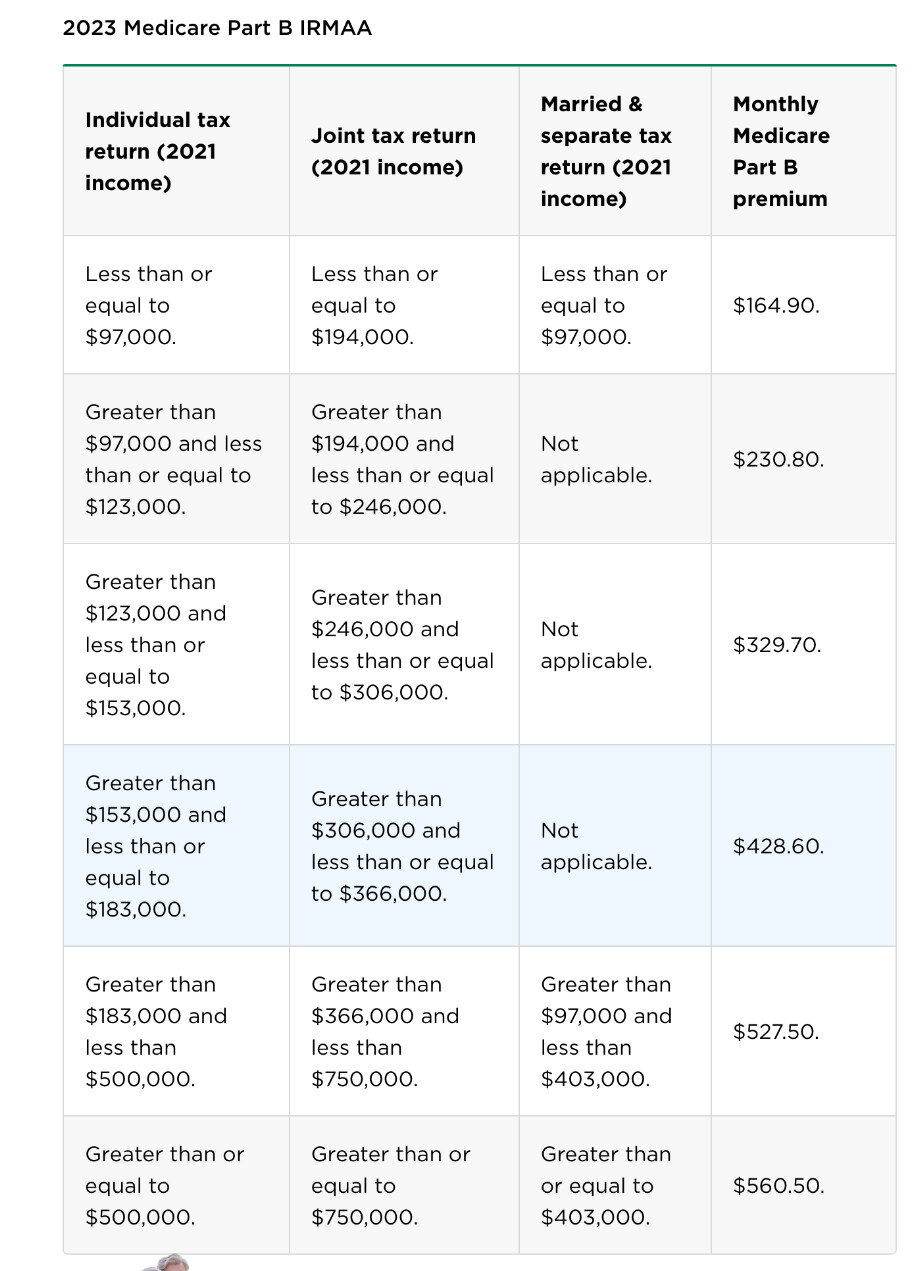

I some about retirement. Oftentimes I read about people talking about keeping income lower to keep medicare costs from being higher. How much are we talking about? From what I see at a quick glance it appears that if you are married you have to make more than $194K to have increased premiums, is that right?

Yes. For the vast majority of people, this is not an issue … they can only wish they had enough income that they needed to pay the extra.

But for those who are retired & not yet eligible for Medicare, keeping income low may allow government subsidies that help lower the cost of their insurance.

So in the scheme of things medicare costs probably shouldn’t be driving the way you structure your retirement. An extra $66 per person a month is probably not worth fretting over.

Agreed. I point out IRMAA because I’ve heard of retirees getting surprised by the impact when doing a large Roth rollover, besides just the extra tax bill they did expect.

For example, if somebody rolled over their full traditional IRA to Roth and it pushed them over $183K.of “income”… the IRMAA impact for married couple (if both over 65) would be 2x362=$724 extra per month for a year. Doing it smaller gulps over a few years could make sense.

IRMAA has a 2 year look back I think. My uncle got caught in it cause sold a bunch of farm land. Really the timing was out of his control but as a single person it hit him hard for the next year until refigured. Didn’t hurt my parents since they had larger margin for increase.

Hit us when husband retired because of unusual stock gain year that didn’t pay attention to but retiring is a reason to appeal. He made a last minute decision on when to retire. Planning ahead when can as far as taking gains, selling stuff, etc can be helpful

I see now. So if you are converting to a Roth from Traditional and do a large amount in one year then yeah you are screwed. But taking $20-$50K in a normal distribution from an IRA probably isn’t going to increase your medicare costs. Of course you are going to have to pay taxes on the distribution, but you didn’t pay any taxes on them in the first place.

If the sum they had was invested now in a index fund (which it won’t be), it would be worth $89 million in today’s dollars in 2063 ($271 million in nominal terms) assuming the same market returns as the past 40 years.

So in 2063 when I’m approaching retirement age, that would be a very large sum of retirement money and maybe I’d have an article written about how I spend that money

So I don’t find that article particularly unbelievable.

That’s the beauty of compounding.

It starts off slowly but accelerates.

In fact, a single $100,000 investment in 1985 would be worth around $6 million today in today’s dollars if it had been put in an index fund then and just held there for 38 years.

One thing I never do is count other peoples money, and I certainly don’t count it as mine. My mother is pretty well off and doesn’t spend her money, though I wish she would and I encourage her to. I don’t plan my life on how much is going to be there for me when she passes on. I doubt your parents would be thrilled with you deciding that the money they have saved now is never going to be spent on them, and will be invested for your benefit. You have no idea what they will do with it in the future, whether they will spend it or give it to charity.

I was just trying to demonstrate the power of compounding using an example so the figures in the news article shared above weren’t out of the realm of believability.

You have no idea what they will do with it in the future, whether they will spend it or give it to charity.

I very much doubt that they’re going to be giving money away. I remember donating some of my money to charity when I was 12 and they practically shouted at me for wasting my money.

I know my parents very well. They’re very, very skeptical of charity as a concept and as a philosophy.

You have no idea what they will do with it in the future, whether they will spend it or give it to charity.

‘There’s no way we’re going to need all of this money so we’re doing this all for you guys [me and my siblings]’

I’m no genius but I can probably ascertain where that money is going to end up considering the things my parents tell me.

There’s 3 possibilities:

Charity - not going to happen as my parents don’t believe in it.

Parents spend it - my parents are fairly frugal people and there’s no way they’re going to spend as much in retirement as they do now.

The kids get it - Dad says it’s either us or the government and he definitely doesn’t want them to get it.

So it’s almost certainly going to be option 3.

I don’t plan my life on how much is going to be there for me when she passes on.

This sounds like something someone older would say as opposed to most young people.

Young people are absolutely planning their lives around inheritances. There have been countless articles written about how young people are anticipating inheritances to pay for things like property and even retirement.

I’m realistic. While I have my own job and will be able to retire by myself, I know my parents’ money is my money. I see nothing rude or presumptuous in this when my parents have told me this.

Most young people do not have parents who are likely to bequeath a large amount of money to them (or anyone) when they die. You may be an outlier in this respect.

Indeed, many young people will have “negative inheritance” if their parents run out of money and need financial (or labor / caregiving) assistance from the younger family members.

But the point I was making is that I don’t see it as rude or presumptuous to assume that I’ll be inheriting that money (they’ve already given us significant sums each).

I love my parents and they talk about the money all time. I don’t feel bad or rude when that’s just the culture I’ve grown up in.

My original comment wasn’t even intending to be about that in the first place but I’d thought I’d address the comment about me making assumptions above.