Well a lot of people were afraid the tax laws were going to be changed in 2021-2023 and they haven’t been. And likely won’t.

1 Like

We are aiming for SS at the recommended retirement age (66 for husband and 67 for me). Decided to keep income down until that time. We will live off of non-retirement savings until then.

1 Like

OK. I’ll play. This one’s for Blossom.

I’m 58. Wife is 52.

home equity is $1.4mil. no mortgage

529s x 3: $950k

401k: $1.4mil

IRAs: $800k

Pension: $5k/mo beginning age 62

aftertax accounts: $2.7mil

Will probably inherit $3-4mil in future.

I’m going to retire at age 62. We’re pretty frugal.

3 Likes

By “frugal”, have you estimated your retirement spending level? That is a very important part of the equation in determining if you have “enough”.

1 Like

From ssa.gov: “Your current or former spouse may receive benefits based on your earnings record. Your spouse’s decision on when to begin this benefit can impact the amount of their spousal benefit. If your spouse begins this benefit between age 62 and their Full Retirement Age, the spousal benefit amount will be permanently reduced by a percentage based on the number of months up to their Full Retirement Age.” (This is from the Plan & Prepare page, which is in the personalized info section after I sign in to MySSA.)

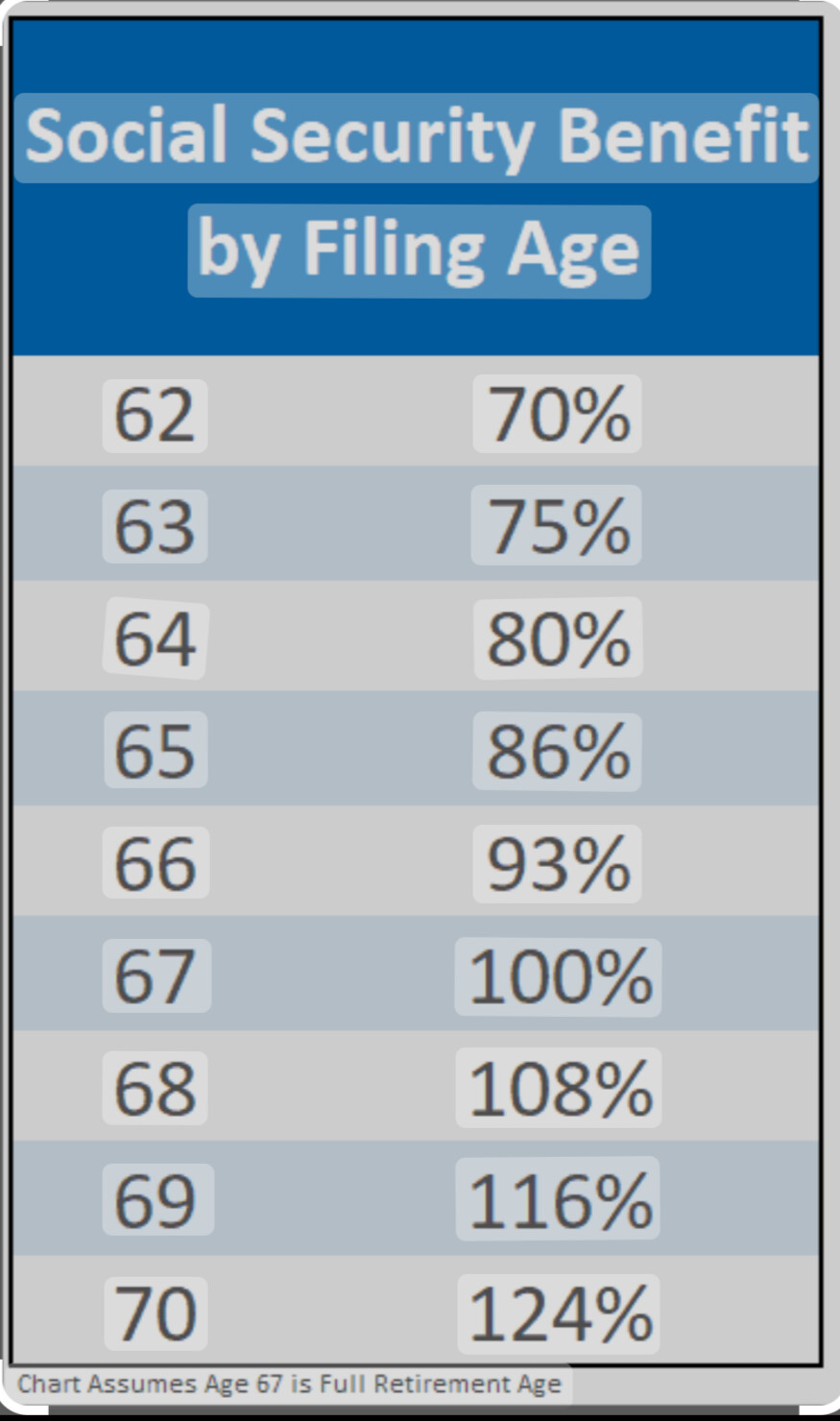

I had planned to take mine at 62 given my lousy actuarials, but if I take a benefit before FRA (67), my benefit – and what I’d get as a spousal benefit because H’s amount will be higher than mine – are permanently reduced. H is working longer and may wait til 70 to max out my benefits (esp survivor benefits). Me taking it earlier undercuts that. It stinks. I wanted to throw it into the bank. OTOH, I probably can’t beat the 8%/year increase for each year I wait.

2 Likes

small nit: the 8% growth is for the years after FRA. The haircut for claiming before FRA is 6.67/yr for the first 3 years, and 5% after. The net is about a 30% reduction if you claim at 62.

3 Likes

30% compared to FRA, or 30% compared to 70?

1 Like

Very helpful chart!

just a nit about FRA (in case folks have heard about friends lower age for 100%):

“If your birth year is 1960 or after, your normal retirement age is 67. Anyone born between 1955 and 1959 has a normal retirement age between 66 and 67 – that is, 66 plus a certain number of months . For instance, if you were born in 1958, your FRA is 66 and eight months”.

5 Likes

Wait — to be clear, you are talking about potentially three separate benefits:

-

Your OWN benefit based on your own earnings

-

Your spousal benefit (50% of your spouse’s benefit). You only get this if it is higher than benefit 1.

-

Your survivor’s benefit, which is the same as your spouse’s benefit that you can assume when your spouse passes away.

I may be wrong, but I believe you can choose benefit 1 as early as age 62 WITHOUT lowering the amount of benefit 3.

One is the benefit on your earnings and the other is the benefit on your spouse’s earnings.

If you take your benefit 1 at age 62, it will be lower than if you took it later. But if your spouse waits until age 70, you can switch to your spouse’s higher benefit (benefit 3) as your survivor benefit if your spouse predeceases you.

At least that is my understanding— if I have that wrong, someone please correct me.

well, if you really want to be clear:

- yes

- technically, you still recieve #1, plus you get any difference between the spousal benefit and your benefit

- ditto. You still get #1, plus the difference between what your higher earning spouse was receiving and your benefit

In other words, you will always receive your own benefit amount. The spousal/survivor is on top of your own benefit, But it all comes in one electronic deposit, so most folks are unaware – and have no need to care – about the different tranches of cash.

4 Likes

I guess it makes me a little sad that if my husband dies before me…I will get zero SS from his earnings…because of the offset and windfall provisions. That will mean about $47,000 a year less income…I think that’s his age 70 benefit. Something close to that. He will be collecting the maximum.

I’m 62, so is H, but I’m six months older. He’s not retiring before FRA (67).

If I take my SS at 62 based on my earnings record, it’s a 30% reduction. I wouldn’t get 50% of H’s SS benefits at his FRA (even if I wait to claim spousal benefits at 67) because I took mine (based on my record) early. That reduction is permanent.

This specific example is towards the bottom of the AARP article, and corresponds to what I read on the SSA.gov site and when I called SSA last year.

I’m thinking I should go into a SSA office and ask questions.

Is maximizemysocialsecurity.com the site folks have recommended in the past?

1 Like

I’m a fan of opensocialsecurity.

click on the check box in the upper middle to add your own details.

3 Likes

That opensocialsecurity.com site is helpful. It does support the advise from our financial planner for our situation (older H - he takes SS at age 70, me at 62).

‘Managing retirement accounts’ takes work…company 401k managed by Prudential had it all go under Empower. So learning the ‘Empower’ system. We had to set up some things as this is our first time to have a direct withdrawal to us (we have done rollovers to Roth IRAs before). So after navigating around, we decided to change two investment choices to the Fidelity 500 Index, with better performance record. But have to wait for withdrawal to take place before we transfer investment choices.

Getting around now to managing personal Fidelity investment account. My two book club books will have to wait a bit longer…

We had a hard time with figuring out SS ages. On my own, I would probably have waited until 70 because I am still working and expect to work well past 70. But, my wife has not had a high income (she’s a painter and had some years where she made money and some where she took losses). So, she was going to base things on my income. I asked our FA and they did a bunch of calculations and it seemed like age 68 for me was optimal for the two of us, but I honestly can’t reconstruct the analysis.

Per @gpo613, I have been able to set things up so our non-retirement assets other than our houses (only one is significant) is in a trust and thus not in our estate. Presumably there will be a big step-up in basis in our house. But even with zero distributable assets, I don’t think it was optimal for me to take SS earlier.

2 Likes

Question about Trusts. Is there a way for an elderly person to set up a Trust such that there is option to sell house and keep proceeds (not have them go to assigned beneficiaries) if the ideal “aging in place” plan does not work out …… and the money is needed for nursing home care?

A relative recently set up a trust like this. Proceeds from sale will get held and used to pay for nursing care if necessary. If not it passes to beneficiaries.

2 Likes

I am not an expert but we have set up a trust and the one thing I learned is that are many, many kinds of trusts. Plus, trust laws differ from state to state. Find the best trust/estate lawyer in your area and consult him/her. Yes, it will cost $$$, but it is worth doing so.

7 Likes