@bennty I do think as the senior ranks grow in number (AARP representing age 50 and above) it will be harder to trim senior SS/MC benefits.

There are many of the younger folks who have no concept of saving for the future; live now. They are so enamored with the entertainment and sports world instead of ‘the real world’. People who have spoiled their children. Some parents who have had no clue how to keep the ‘culture’ from adversely affecting their children. I have two younger siblings who ‘lost their way’ in many areas – the youngest ‘playing with fire’ and lost – convicted felon/non-violent crime (gambling/bookie).

That concept about making more money as you get older - that depends if you are willing to often make a lot of changes to earn more. Many don’t have the skills to advance; and then there are the growing number of places who will find a way to get rid of higher paid employees w/o reason for s/k/a.

Yeah, see, I think this is going to cause some trouble for older folks.

The problem isn’t that the kids are blowing all their money on avocado toast and weekends in Portugal, or on drugs. The problem’s that they don’t have money to save. They’re 25, deep in debt from school (no, please don’t go on the circuit about the choices they could’ve made instead; they really couldn’t, the options posited didn’t exist as real options), and then they’re 35, still renting, with nothing; and then they’re 40, still with nothing much and already starting to get passed over in favor of new graduates who’ll work for even less and have exciting fashionable new skills and vocabularies.

They went to law school and found out the hard way that the market for lawyers was not as advertised – but they still have law school debt.

They went to master’s programs and found they got snookered there, too, and have giant debt from combined undergrad/grad.

They saw grad school debt as a trap and avoided but have trouble getting past entry-level jobs and are effectively clearing $18/hr plus some manky benefits, and still have $14K in school debt, or married someone they loved and is a good person but has $85K in school debt and makes $40K/yr.

They don’t have the money for saving. As long as older folks struggle to come to terms with that reality, they’ll be slow to recognize how the old-age money landscape is likely to change.

AARP will be functionally irrelevant, voteswise – just not enough people. It’ll still be a voice, but it won’t be what it is today. Gen Z, Millennials, very large generations; Boomers will mostly have died, Gen X is small and has started dying.

I feel compelled to say it’s not just younger kids who are “live for now” etc. There are plenty of boomers who did and are continuing to do the same thing. There are many many people of all ages who haven’t saved much for retirement.

My son (25) was calling me stressed recently because he didn’t have “enough” saved for retirement. He has more saved now than I think I had when I was 40, for real. He is doing great, and living below his means.

Some other kids I’m very familiar with, not so much. They spend every penny and look to mom and dad for help often.

@bennty - Can you explain your comment more? The IRMAA table screenshot I posted above is for annual income, not assets. Trying to understand your point better. (My question is for group education… no gaming needed in my situation.)

@bennty my two DDs had no school debt. Studied in careers where they could get a good job with UG degree (nursing and engineering). They both are smart and hard working - nurse (27) is in first level management and is a key employee according to her bosses (the head of the hospital is concerned about how well things will go while DD is out on maternity leave for 12 weeks - she is on so many committees and has such leadership – DD is starting maternity leave a week before her due date and plans to work a very full week/OT just before then to have all transitioned to other people and leave no loose ends). DD2 (25) double majored and after basic civil eng work experience for 3 years won a job with a design firm where she can use both her civil eng and her architectural eng s/k/a. DD1 helped her DH get out of his school debt and he is working on career traction (he had goals that didn’t pan out). DD2’s BF is 24, working off school debt, and gaining entry level experience in his field – IDK if he is going to make it beyond BF/GF with DD; time will tell.

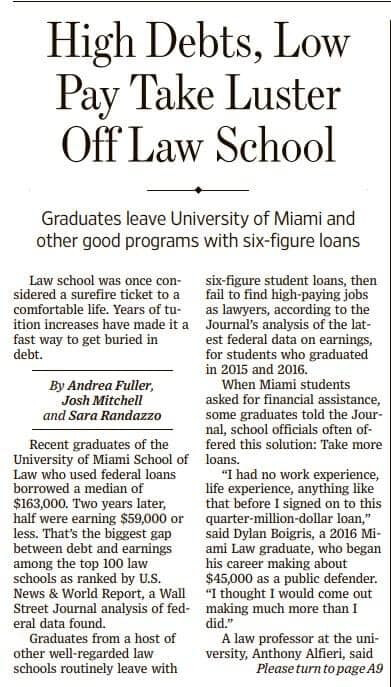

You hear about the ones that have taken on a lot of debt and not making the money to pay it off - their parents had to help shape their thinking. There is a facebook thread on “Paying for College in a Financially Sensible Way” and other groups that share information to help parents navigate college costs - and IDK the date of this article “High Debts, Low Pay Take Luster Off Law School – Graduates leave U of Miami and other good programs with six-figure loans” – saw it from a law graduate’s parent who knew to keep debt very low.

There are some very good points made in this article. “…students tend to be unsophisticated borrowers, with many taking out the maximum every year – they don’t know how to manage money in large numbers, and so over a relatively small period of time borrowing got out of control”. Two clusters of starting attorney salaries $45K - $75K for public service and small firm attorneys, and around $190 K for large firm jobs. “Undergraduates who finished law school in 2019 earned a median $72,500 according to the National Association for Law Placement. That is about the same as graduates who finished school a decade earlier earned soon after graduating.” “At lower ranked but still competitive American University, graduates borrowed a median $175K, nearly triple their median earnings after two years.”

Parents have to be aware of the paradigm shifts and how all the surrounding changes affect them and their children/grandchildren. Many on this thread are in the sandwich of having elderly parents/relatives that need care with limited resources, and students/young adults who are navigating their education and career with lots of decisions – along with risks and threats, opportunities and rewards. I remember back when DH and I were starting out right out of college - we navigated and observed; learned things we are now teaching to DDs.

I know parents who spend down their own funds or take out ridiculous parent plus loans for a student to go to ‘dream school’ for UG when they truly cannot afford this risk to their retirement funds.

If benefit cutoffs or price tiers are tied to income, people will often try to control income so that it stays within certain bands. ACA, for instance, is income-tested, as are lots of tax benefits. You can have a low income and high assets and still get major subsidies for marketplace health insurance under ACA. But means-testing also generally includes assets. This is common for welfare programs: for instance, if you have anything worth anything, even a car you can sell for a few thousand, it’s nearly impossible to get SNAP, regardless of your income. That’s why it was so alarming when over 15% of the US population was on food stamps during the Great Recession – you have to be genuinely destitute for that. A whole lot of kids were in that position then, and they’re now young adults, voting age.

When Medicare goes means/asset-tested, it won’t really matter what your income is if you’ve got substantial assets. Say your joint income in retirement is under $176K, but you’ve got $2M in assets. You can expect, under asset-testing, your monthly premium to go up substantially. And the rationale there is, look, you’ve got hella bank, you can afford it. It’s not like you’re hand-to-mouth.

So if your plan is “have lots of assets for security, but show up on the Medicare radar as low-tier income”, I would not expect that strategy to hold. I don’t see it falling apart immediately, but I don’t see the kids going for supporting that longterm.

essentially what you are suggesting is wealth tax, correct? Assuming it passes Constitutional muster — which it may not – such a tax is administratively difficult (and costly) to implement. Doable, certainly, but much more intensive work required than just assessing a higher % of reportable income.

Looked at from the other side, it’s a rollback of wealth subsidy. And it’s not that complicated to do. All it means is that the lines change for the tiers, which will likely have new numbers attached to them.

Say that right now your joint income in retirement is $80K, but you’ve got $5M in assets. Under current rules, you’re in the lowest Medicare-premium tier: your income is the only thing that matters. Under new asset-testing rules, you no longer fit the lowest tier; maybe you’re second-from top, which is now $800/mo.

They’ve already got your banking info, so they can leave this to you to self-report and decide whether or not you want to risk an audit, same as they do now for welfare benefits.

EITC actually uses a strategy I can see coming into play: there are earned-income and investment-income cutoffs. I think max investment income under EITC is around $3500. If you’re a retiree with a pin-money job, Soc Sec, and a bit of ordinary-office-worker 401(k) money coming in, fine. If your retirement and other accounts and properties are banging, though, your gains exceed cutoffs for low-tier pricing, and you’ll be rolled into higher-tier bands.

That would indeed be more complex and expensive on the taxpayer side, and I can see things getting messy when inevitably some reps want unrealized gains counted, but in the end, people with that kind of money would in the main have enough to absorb the cost without much more consequence than a bad mood, and it’d allow for the kind of larger, unexciting retirement bankrolls that working stiffs tend to want. It’d also have the effect of discouraging casino habits among investors.

The question is, how does one value assets? Sure, a bank and broker can provide a 12/31 balance statement for publicly-traded companies, no problem. But what about the millions of folks that have small businesses? How does the IRS value a private business? How do they value your farm? Your two-plex rental? Your home? Your car? Your diamond/art collection? Your bitcoin? Your life insurance policy? Your annuity?

If you are gonna leave this to the IRS to audit, they have to have some way to do it…(hint: this is one big reason why many Euros have dropped their wealth taxes.)

Well, don’t forget that the old and moneyed will be many fewer than they are today, with considerably less political power – again, barring autocracy. So if the kids say “look, we’re going to make this simple, live with it,” that’s what you’ll be doing.

There are already standard ways of doing all those valuations. My guess is that if they went that way, standard protocols would be anointed, and it’d be up to the angry taxpayer to fight it and say it’s not fair in this instance. I don’t think, though, that if you’re arguing that the IRS is valuing your diamonds and art high and should be cutting you a break on your Medicare premium, you’ll be getting a lot of sympathy in the land of 2040.

Again, keep in mind all those student loan balances, the kids who’re trying to see a way through school now without giant debt, and those kids whose parents qualified for SNAP in 2009. Those will be the middle-aged people running the show in 2040.

Except that wealthy people who would presumably be taxed with a wealth tax would presumably have all kinds of creative ways of hiding wealth from being included in tax assessments, unlike poor people who may get SNAP who have much more limited types of assets and means to hide them.

I.e. basically a similar situation as with the income tax – most people with typical levels of income have fairly simple and well documented income that is reported on W-2 and perhaps 1099-INT/DIV/B forms, so taxation is relatively straightforward. But there are many more ways that wealthy people can try to hide income; much of the complexity in the tax laws comes from how to assess taxable income (including explicitly stating that it is to be reported and taxed, or the effects of lobbying for exemptions, deductions, credits, or special favored rates).

Of course, there are some people with ordinary levels of income (or wealth if we are talking about wealth tax) who do get caught up in the more complex taxable income (or wealth if applicable) calculations, such as those running small businesses.

People. This is not a wealth tax. It’s no different from what already happens when figuring out who gets food stamps.

Ya got big assets, ya don’t get big benefits. That’s all. Reduction of subsidy for your health insurance.

Of course, if you don’t think assets should be figured into food stamps, housing vouchers, LIHEAP, and a raft of other benefits, please get behind that politically. It’d sure help.

However, defining “wealth” for the purpose of reducing Medicare subsidies or whatever is still subject to the complexities of finding all of the ways that wealthy people may hide wealth (much the way they try to hide income from taxation).